by Brad Houle, CFA

Principal

Head of Fixed Income

Portfolio Management

This week, we sent the following communication to all Ferguson Wellman and West Bearing clients in response to heightened market volatility. We felt that this message was also appropriate to reiterate for our weekly blog.

When we presented our 2025 Investment Outlook to clients earlier this year, one of our key points was that there was going to be a lot of noise and rhetoric surrounding tariffs. Our view was that the rhetoric would be worse than the economic impact.

While U.S. markets expected an onset of tariffs this year, what is agitating investors is the uncertainty regarding implementation as well as the view that tariff rates, once enacted, are going to be higher than originally expected. The current rate of change in Washington D.C. only adds to the concern over what the regulatory environment will be going forward. We acknowledge that regardless of political affiliation, the amount of and speed at which these changes are occurring can be jarring. This uncertainty has spilled over to consumer and business confidence, leading economists to lower their estimates for GDP growth in 2025. This result is a classic growth scare, creating a “risk off” environment resulting in a roughly 10% pullback in the S&P 500 over the last three weeks.

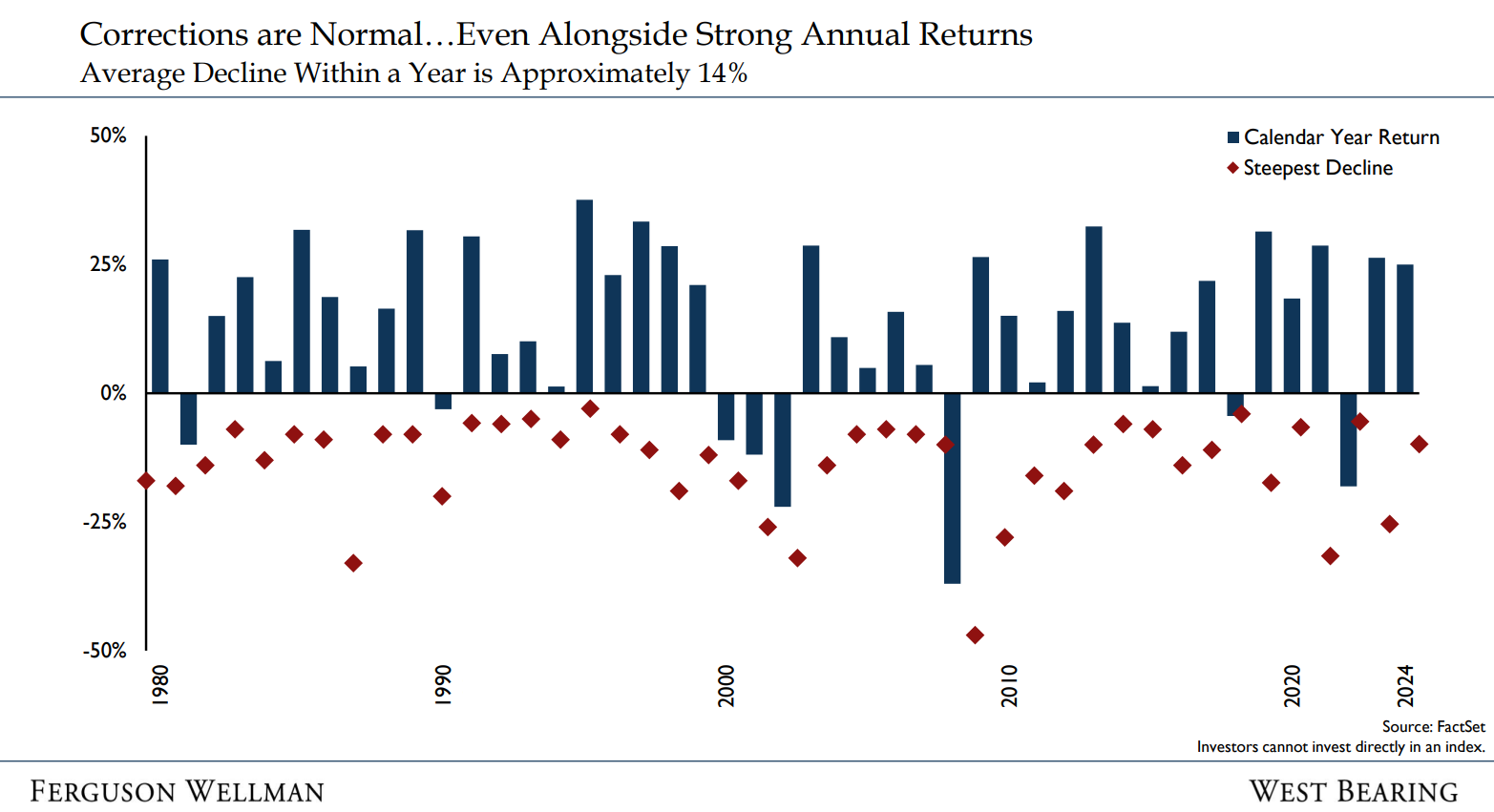

This Has Happened Before

Source: FactSet

Declines are common. In any given year, markets experience declines of close to 15% (on average) as seen in the chart above. Additionally, since the lows of March 2009, there have been 29 pullbacks, each at least 5%, with the 30th occurring this month. What’s important to consider, however, is if this is just a “common pullback” or something that indicates a recession. Currently, we do not expect a recession in 2025. The jobs report last week still showed a healthy employment picture and weekly unemployment claims continue to remain at historic lows. In addition, the Consumer Price Index for February was lower than expected, with inflation dropping down to 2.8%.

What Ferguson Wellman is Doing

During this environment, the best antidote is a diversified portfolio. As we discussed during our investment outlooks at the beginning of this year, we expected bonds to act like bonds during the next stock market correction and appreciate in value. Our expectations have been correct so far, with bonds appreciating in value and mostly offsetting the declines in stock prices in balanced accounts.

What the market is looking for is a timeline for tariff implementation as well as tariff magnitude. There’s no question that the tariffs will have an economic impact; what we should be considering is if the impact will be concentrated in the auto and steel industries, or if it will be more widespread. Until there is more visibility on that, expect higher volatility. It is our belief that economic growth will remain positive, with the worst-case scenario playing out as 1.5% of GDP growth and just over 3% inflation for 2025. We will also be paying close attention to any change in consumer spending, as well as the employment rate.

Therefore, at this time, we are not making any asset allocation changes to client portfolios.

Takeaways for the Week

We acknowledge that the current political environment has been jarring for investors and created market volatility

We believe we will not have a recession in 2025 due to the strength of the labor market, continued GDP growth and a resilient consumer