by Alex Harding, CFA

Vice President

What does that really mean for you?

Last week, the Federal Reserve made headlines after raising their benchmark interest rate by 0.25%. This week, the Fed remains in the spotlight due to comments made by Chairman Jerome Powell at Monday’s National Association for Business Economics annual conference. In his speech, he highlighted the strength of the labor market while acknowledging inflation has not cooled as forecasted. He also noted the Fed would move “expeditiously” to return towards neutral monetary policy. Said differently, the economy is in a position of strength; it’s time to raise borrowing costs and transition away from pandemic-induced stimulus. In response, U.S. Treasury yields continued their climb higher this week.

What is the federal funds rate?

The overnight interest rate charged by a bank for lending excess cash to another bank. The Fed sets the target range (currently 0.25% - 0.50%) but the actual rate is negotiated by banks daily.

How does this impact you?

Although the fed funds rate is specific to interbank lending, it has a trickle-down effect on the rest of the economy. For example, hours after the Fed move last Wednesday, financial institutions such as Wells Fargo and Bank of America raised the prime rate from 3.25% to 3.50%. The prime rate is the rate of interest charged to a bank’s most creditworthy customers. It is used as the base rate for many types of variable-rate loans such as credit cards, home equity lines of credit, margin accounts and small business loans. Though a 0.25% increase may seem inconsequential on a standalone basis, the market is currently pricing in eight more federal funds rate hikes, bringing the target range to 2.25% - 2.50% by year-end. At those levels, individuals and businesses will feel the impact on outstanding loan balances.

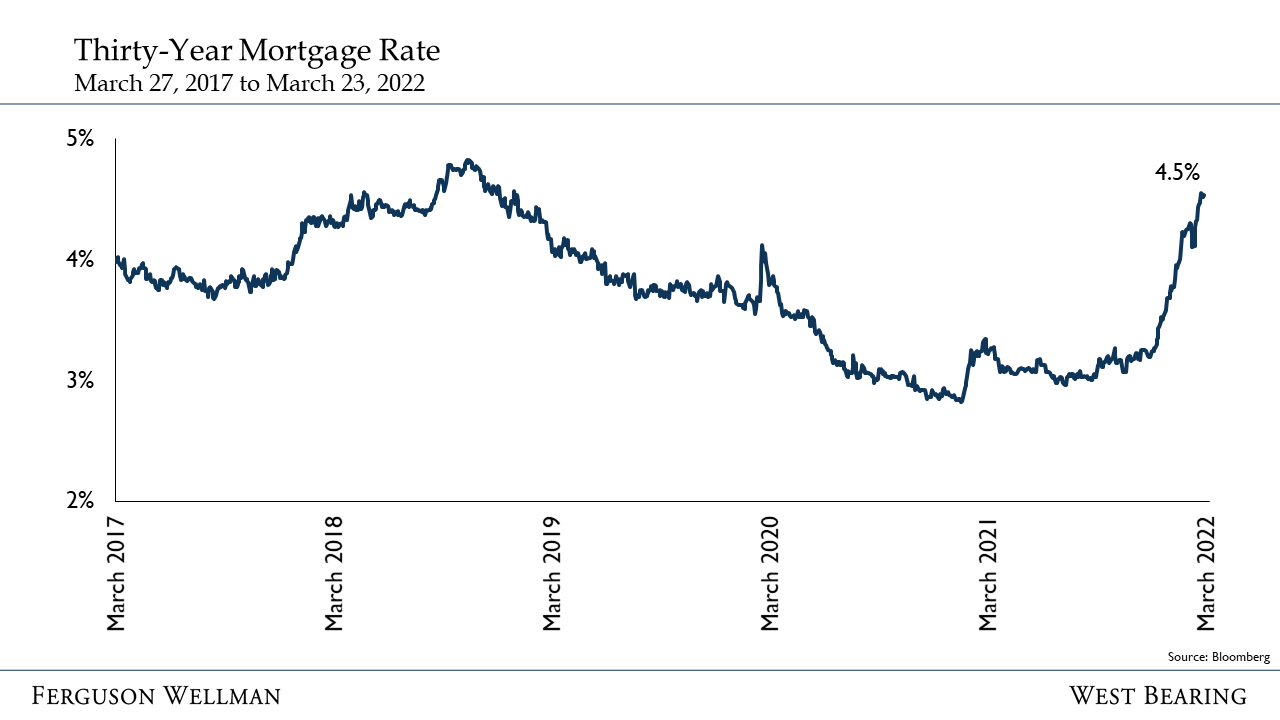

Mortgages are typically structured as a fixed-rate loan with the interest rate being influenced by several factors. If you are looking to purchase a new home, you will notice mortgage rates have moved more than 1% higher since the beginning of the year as the industry has been anticipating interest rate hikes and pricing in higher inflation. Higher mortgage rates should slow housing demand and the speed of price increases.

Source: Bloomberg

Savings accounts earning an average of 0.06%* will see rates move higher, but it won’t be immediate and less than the increase in borrowing rates. The reason? Financial institutions are flush with cash and do not have to aggressively compete for customer deposits at this point in the cycle. The wider the spread between what a bank pays for deposits and what they charge on loans boosts revenues and is one of the reasons we are generally overweight the financial sector within client portfolios.

*Source: BankRate.com

Our Takeaways from the Week

Borrowing costs are going up - now is a good time to review the structure and terms of your loans to avoid any surprises

The early stages of Fed tightening have been a “sell the rumor, buy the news” event for stocks