by Shawn Narancich, CFAExecutive Vice President of Research

by Shawn Narancich, CFAExecutive Vice President of Research

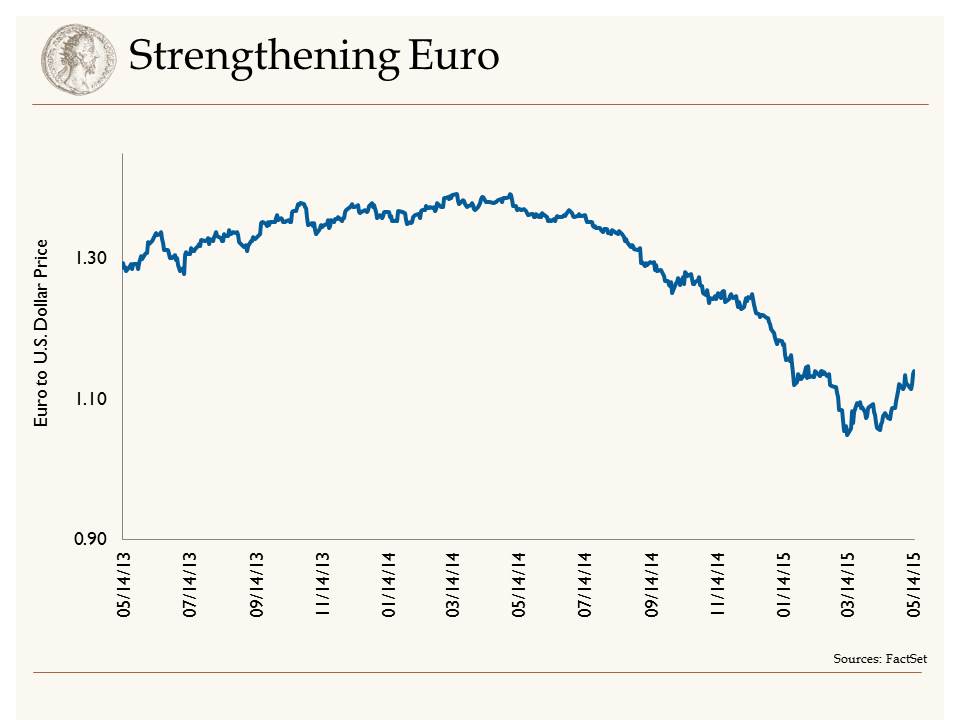

Too Much of a Good Thing?

As Europe begins to make a down payment on its one trillion euro quantitative easing program, the U.S. dollar’s rapid gains have become parabolic and begun to take a dent out of investors’ U.S. stock portfolios. A strong currency is commonly cited for its endearing qualities of reducing inflation and attracting investment, but with the trade-weighted dollar up almost 25 percent since last summer, more and more companies are watching their bottom lines suffer as foreign profits get translated into fewer dollars. We would observe that when an asset’s orderly gains begin to rise at an accelerating rate, the asset is beginning to resemble a bubble, regardless of whether it is tech stocks in early 2000 or the dollar at present.

Bidding Adieu to ZIRP

Because the U.S. economy continues to outpace those of other developed nations at a time when the Fed is preparing to raise interest rates, we aren’t calling for a top on the dollar, but we do believe it is due for a breather. What we would conjecture is that the best of the greenback’s gains may have already been realized, acknowledging that while the Fed’s mandate to promote full employment is being realized, it is in danger of falling short of its other goal, that of maintaining stable prices (defined roughly as two percent inflation). We envision lift-off from the Fed’s zero interest rate policy (ZIRP) later this year, but with inflation increasingly subdued at the imported goods level in addition to that caused by lower oil prices, the Fed is unlikely to tighten as aggressively as the dollar would imply.

Skate to Where the Puck Will Be

We observe in bemused fashion the financial press waxing bearish about the supposed lack of storage capacity for U.S. oil production. Yes, storage builds have occurred at the Cushing, Oklahoma delivery site for the commonly quoted West Texas Intermediate (WTI) oil contract, as an unusually large amount of refining capacity has been temporarily idled for seasonal maintenance and one northern California refinery is offline because of the United Steelworkers’ refinery strike. This too shall pass. With gasoline refining margins now surpassing the robust level of $30/barrel (thanks to strong demand stimulated by low pump prices and discounted WTI oil), refiners are heavily incented to return idled capacity as soon as possible.

Always Darkest Before the Dawn

Are oil prices at a bottom today? Markets tend to overcorrect on the way up and do the same thing on the way down, so although fundamentals of the oil market don’t appear to support $45/barrel oil for any substantial length of time, the price of oil could go lower in the next month or two. But we don’t manage client portfolios with a one or two month time horizon and what we will say is that this cycle is playing out just like we would expect. U.S. drilling activity has plummeted in response to low oil prices, down 42 percent since September, while demand for gasoline, diesel and jet fuel hasn’t been this robust in years. By our estimation, faster demand growth and U.S. production that we believe is set to begin declining are the key ingredients to a recipe for higher prices in the second half of this year. Being overweight energy stocks has not felt good lately, but we are confident that the bearish headlines on oil herald something much more constructive for energy investors.

Our Takeaways from the Week

- Increasingly heady dollar gains are beginning to negatively impact U.S. stock prices

- The most recent declines in oil appear long in the tooth

{kind=link}