by Jade Thomason

Equity and Fixed Income Trader

As February draws to a close, so does our first quarter outlook season. We enjoy hitting the road and sharing our 2025 Investment Outlook with clients and colleagues, and are grateful for the chance to come together and look forward to what's ahead. While this was one of the quieter weeks for economic and market news, there were two releases of note: the Federal Open Market Committee (FOMC) minutes and the January housing data.

The FOMC holds eight regularly scheduled meetings during the year, and at their late January meeting, they unanimously voted to keep the federal funds rate unchanged at a range of 4.25%-4.5%. On Wednesday, the meeting minutes were released which prompted investors to search for clues regarding future decisions and gauge the overall temperament of the committee members. The minutes took a hawkish tone and stated that officials are in no hurry to resume loosening monetary policy, even though most agreed the current policy stance is restrictive. Additionally, it was recognized that “the month-over-month inflation readings in November and December had exhibited notable progress toward the committee’s goal of price stability,” but “other factors were cited as having the potential to hinder the disinflation process, including the effects of potential changes in trade and immigration policy as well as strong consumer demand.” The elevated uncertainty prompted the committee to take a careful approach when considering additional adjustments. Their call to keep rates steady was no surprise, but it is valuable to learn what committee members discuss prior to making the final decision.

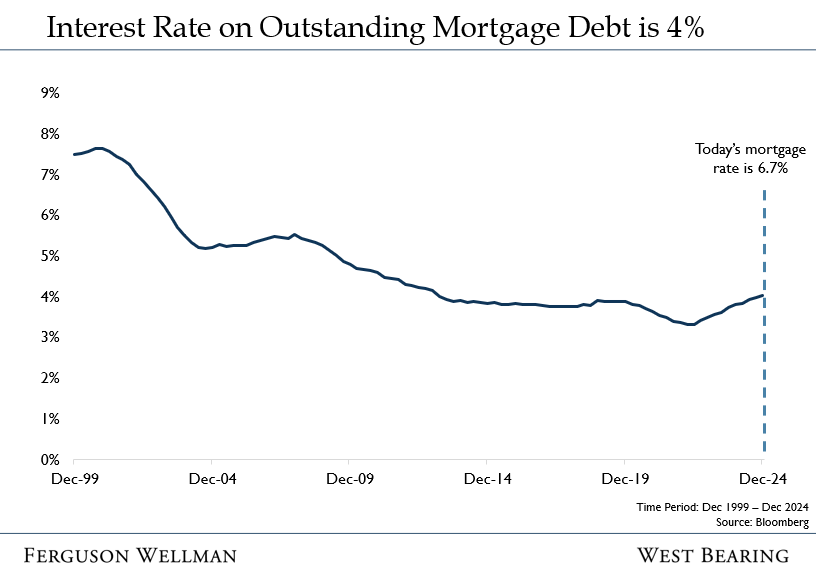

The frequent discussion of rates may be repetitive to some, but to future homebuyers, rates are top of mind and can influence their thoughts regarding home ownership. One important caveat: all interest rates are not created equal. The federal funds rate sets borrowing costs for shorter-term loans, but fixed rate mortgages track the 10-year Treasury yield. The 10-year treasury yield, and therefore mortgage rates, are not determined by the federal reserve but rather, are influenced by the markets’ expectations for economic growth and inflation. Today, the average interest rate for a 30-year fixed rate mortgage is hovering near 6.7%. Shown below, the rate on outstanding mortgage debt is nearly 4%, so many homeowners are locked in and staying put, keeping the housing market tight.

To compound this issue, U.S. housing starts slowed in January as builders pulled back on both single and multifamily home construction. Disruptions from snowstorms and freezing temperatures are always a factor in these winter months, but a rebound will likely be limited due to worries over mortgage rates and uncertainty around economic policies. As existing home sales remain low, and new construction slows, the housing market will have a high price of admission to new homebuyers and those looking to move.

Takeaways for the Week

Another housing metric, existing home sales, fell 4.9% in January from the prior month.

U.S. consumer confidence slid this month and was unanimous across groups by age, income, and wealth. The University of Michigan’s index of consumer sentiment decreased from January’s 71.7 to 64.7.