by Ralph Cole, CFA

Executive Vice President of Research

by Ralph Cole, CFA

Executive Vice President of Research

Take Your Time

Greece and Euro Area finance ministers reached a tentative agreement Friday to buy time for Greece to get their financial house in order. The EU has agreed to provide liquidity for up to four additional months if Greece provides a sufficient list of measures they are willing to undertake.1

Greece will have a primary budget surplus in 2015 which means they will have a budget surplus - if you don’t count debt payments. While this may seem unrealistic, it does mean the Greek government could continue to operate if they stop paying their creditors. However, this would not be in the best interest of anyone. Greek bonds would drop in value, as would some of the bonds of other peripheral countries. This situation is known as financial contagion. Greece in and of itself is not a huge economy (it is approximately the size of Indiana), but the world is trying to judge the effectiveness the European Union. Can they hold it together?

We believe that the EU can indeed keep it together in the near-term. In the future, it may be in the best interest of some countries, Greece as one example, to move out of the Eurozone. If a country finds itself politically unable to work within the confines of the European Union, they may want to exit the agreement in order to control their own budgets and currency. The EU would rather have this happen during a time of strength, rather than at a time of ongoing economic stress.

Waiting on a Friend (Fed)

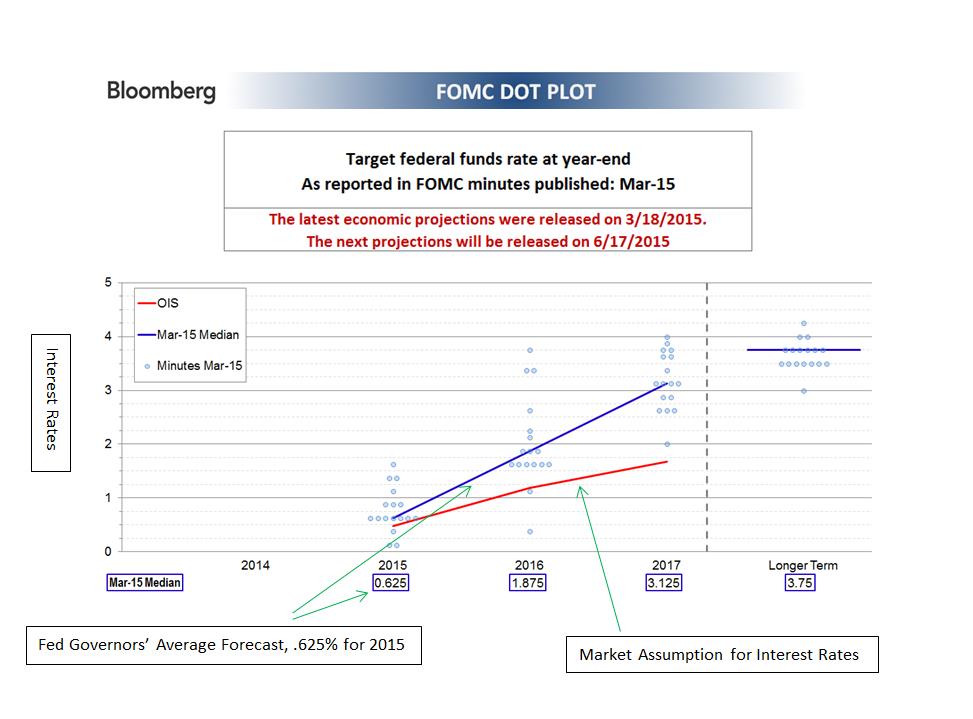

The Federal Reserve board meeting minutes were released Wednesday and markets deemed them to be dovish; meaning that the Fed is afraid of raising rates too soon and choking off a fragile recovery. The surprise to us is that people continue to refer to this as a recovery. Both U.S. GDP and the S&P 500 are at all-time highs and the U.S. passed through recovery territory years ago. While nothing is a foregone conclusion, we believe the Fed will raise rates later this year. There will be a lot of hand wringing over the first Fed rate hike (there always is), but we believe the economy is on very sound footing and can handle higher rates. While it could happen in June, it will most likely happen in the second half of the year. This topic will be discussed ad nauseam throughout the year, but we view tightening as a positive. A rate hike will be a signal to the markets that the financial crisis is officially behind us and extraordinary measures of liquidity are no longer needed.

Takeaways for the Week:

- The Greek debt story is not over, but they do have more time

- We expect the Fed to raise rates later this year

1 Source: Bloomberg

Disclosures