Oregon stocks stumble as market plunges

by Matthew Kish

The stocks of 18 of Oregon's 20 biggest public companies dropped Monday as the stock market tumbled. The S&P 500, Dow Jones industrial average and the Nasdaq Composite each closed down nearly 4 percent.

Northwest Pipe Co. (NASDAQ: NWPX) and Lattice Semiconductor Corp. (NASDAQ: LSCC) were the only large Oregon stocks to post gains. Each ended the day up less than 1 percent.

While there's no consensus on the market stumble, local analysts pointed to weakness in the Chinese economy and uncertainty about central banks and interest rates.

"I would venture to guess it’s more people being skittish about the direction of the Fed right now," said Chris Abbruzzese, chief investment officer for Portland's Rain Capital Management. "The Federal Reserve is going to be less supportive of equities markets going forward.”

They also said the market was due to hit a speed bump.

"The markets had been unusually stable and had come up quite a bit over the past three years," said Kraig Kerr, a senior vice president and financial adviser at D.A. Davidson in Portland. "So most people were expecting a correction at some point and were surprised it hadn’t happened earlier."

Shawn Narancich, executive vice president of equity research and portfolio management at Ferguson Wellman Capital Management, said the firm doesn't see anything "sinister" happening.

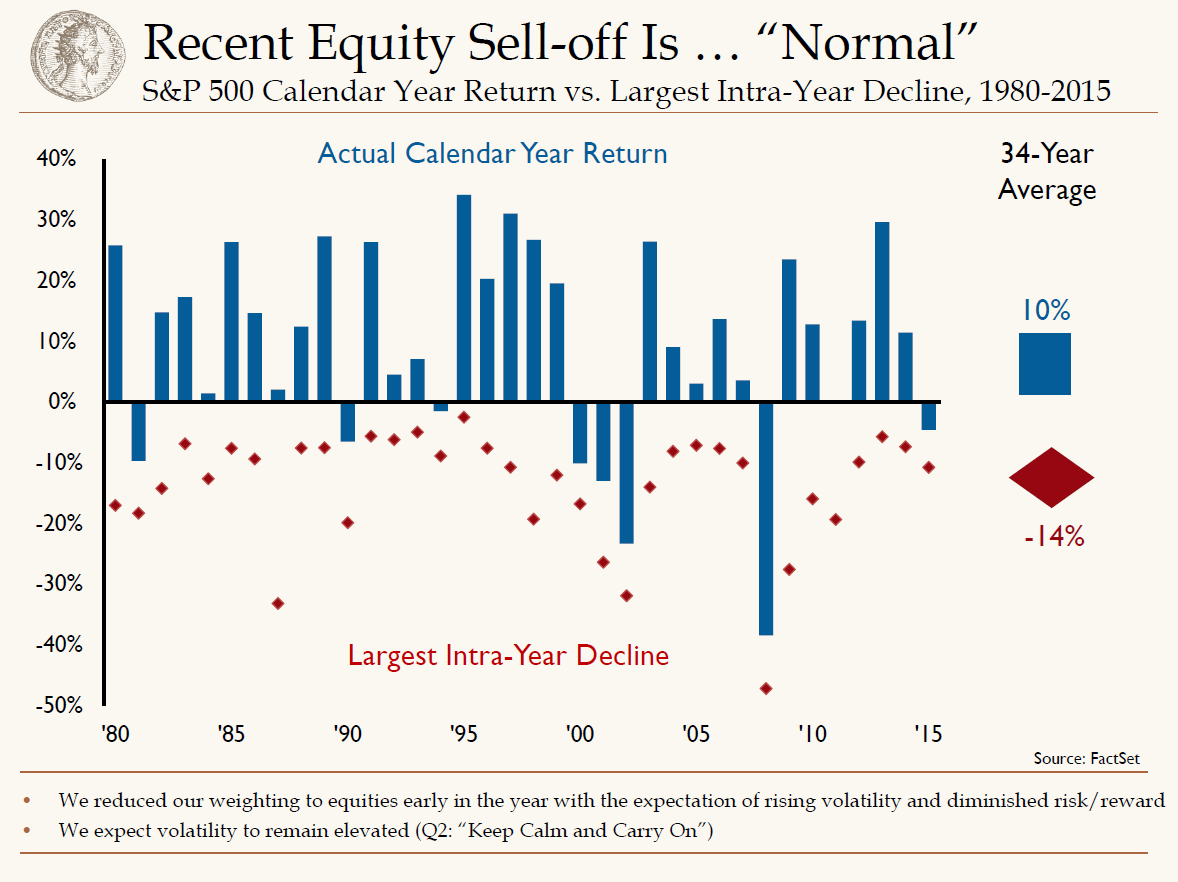

"Our mantra continues to be keep calm and carry on," Narancich said.

Ferguson Wellman expects the U.S. economy to continue growing in the second half. The economy is adding jobs and inflation is low. Consumer spending, which accounts for roughly 66 percent of the economy, remains strong.

"Gas prices are going to start dropping," he said. "Unemployment is low. Disposable incomes are up."

Rain Capital’s Abbruzzese said there’s also “quite a bit of evidence” that “we’re due, if not overdue,” for a resurgence in spending on capital projects that would stimulate the economy.

Kerr said D.A. Davidson's advice for clients depends on circumstances.

"Clients that are going to need cash in the near term may want to consider locking in gains," he said. "For the most part if a client has a well balanced portfolio we're not doing anything."

Abbruzzese said Monday's market volatility highlights the need for investment strategies that minimize risk.

“This is the type of market where we really thrive,” he said. “The approach thrives because we are more mindful of risk factors in portfolio construction.”

Here's a look at how Oregon's biggest stocks fared:

Nike Inc. (NYSE: NKE) — down 2.81 percent to $103.87

Precision Castparts Corp. (NYSE: PCP) — down 1.95 percent to $228.85

Lithia Motors Inc. (NYSE: LAD) — down 2.82 percent to $101.89

StanCorp Financial Group Inc. (NYSE: SFG) — down 0.85 percent to $112.59

Schnitzel Steel Industries Inc. (NASDAQ: SCHN) — down 2.66 percent to $16.10.